Independently from new regulations Transport & Logistics companies are liable for the cargo

After a long-lasting debate in EU the so-called Macron law was put in force after several local implementations were applied on national level. Firstly, Belgium and France followed by other countries banned the opportunity for truck drivers to sleep in the truck cabin, although all manufacturers applied all necessary conditions for a comfortable rest in the vehicle.

The law is seen in the majority of CEE countries as a discriminating enforcement by Western European governments who made their best to decrease the aggressive competition of Eastern European transport companies dominating the transport and logistics market in the last decades especially after the EU expansion in Poland, Baltics, Romania and Bulgaria. Besides it brings many problems for the insurance industry, due to compulsory absence of drivers out of the vehicles in certain cases especially when regulating their resting slots.

This article focuses on the special hot topic directly or indirectly connected with the new regulations on the market – robbery of cargoes or total theft of vehicles increased in numbers as a logical tendency to above legislation changes!

From theoretically good intentions to chaos in practice

A problem with many unforeseeable aspects as a ticking time bomb was initiated on May 31, 2017, when the EU Commission published a large “Mobility Package” that aims, among other things, to make a number of changes to Regulation (EC) 561/2006 with regard to travel and rest times. For example, a change was proposed to the effect that the weekly 45-hour rest period or any other longer rest period must be spent in appropriate accommodation with adequate sleeping and sanitary facilities. So, sleeping in driver’s cabs should therefore be impossible across the EU for the longer compulsory resting time.

After many months of discussions, disputes, strikes by transport and logistics business also directly in Brussels regarding the above changes and other restrictions mainly on more frequent trips back to and from homeland, the law was practically put in force. One of the major consequence of this is that drivers will either spend their weekly rest periods in accommodation provided by or paid for by the employer or – if it can be arranged – at home and the trucks will therefore have to be left alone. And here it comes to the major point for the insurance industry: What if a truck and its goods are stolen from a trailer during this period?

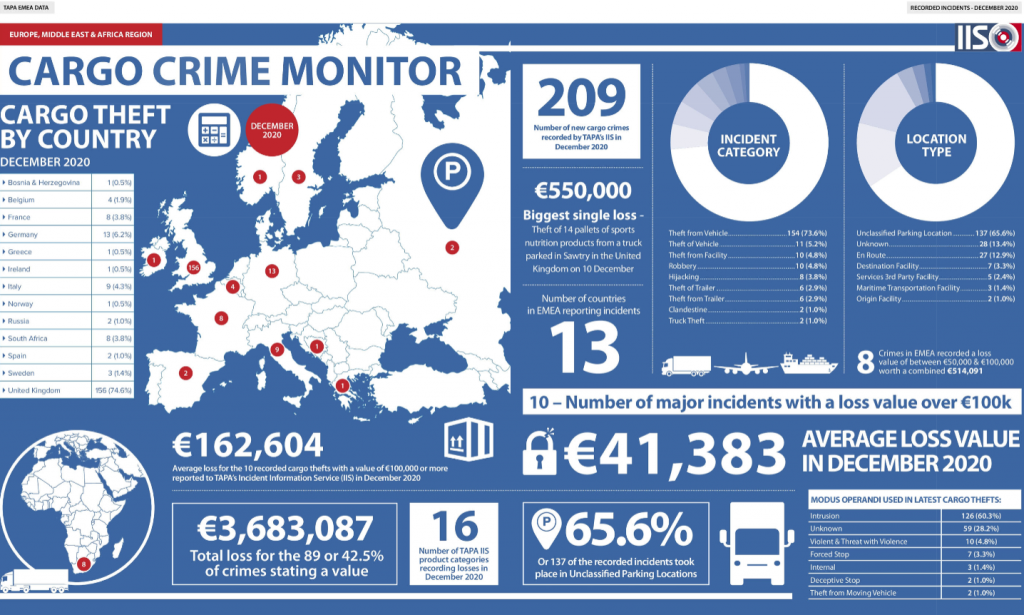

But let us firstly look at the major insurance problem: It is not a secret that theft and robbery have been major risks in the transport and logistics industry for many years already (more than 15.000 theft/robbery cases p.a. in Europe!). In addition, the illegal immigrants are also an issue! Based on data from Transported Asset Protection Association (TAPA) we see a significant increase of cases within last years – a special focus is given on the fact that more than 65% of cases of theft happen on unsecured parking (TAPA latest report December 2020).

We should also not forget that nevertheless of EU efforts to work on providing more and more secure parking lots their number is still insufficient to the increased traffic and the demand on industry side to use such facilities especially after new regulations are being implemented. A critical issue is that even if a transport company makes its best to plan, choose and try to use secured/guarded parking lot, the number of all fully compliant to the insurer`s requirements locations is very limited and often fully booked and impossible to make use of. And who does and how actually define what a secured/guarded parking lot means? There is no exact and common definition for this!

A Pandora box opened for unforeseeable increased risk cases!

The above then clearly describes the challenging development of the industry on one side and the dilemma of how to protect against the theft/robbery risk while at the same time a transport/logistics company is liable (also unlimited in case of gross negligence equal to willful misconduct of its drivers – Art. 29 CMR!) for damages and theft of the cargo and when at the same time drivers are not allowed to stay with their vehicles in certain cases for a longer period of time. However, an important question arises out of above: Where is the role of the respective insurance cover – a carrier`s and freight forwarder`s liability insurance should be enough, shouldn`t it?!

The answer is very tricky from Insurance industry’s point of view as in many of the cases, especially in CEE insurers simply apply restrictive coverages for keeping up the loss ratios low without taking into consideration that long term relationships with customers cannot be built by only increasing exclusions in wordings. Many CMR insurance policies contain provisions that can be extremely sensitive for carriers; the conditions vary from insurer to insurer and can include, for example, the following clauses:

As you can see, there is no limit to the imagination of insurers when it comes to exclusions. Some policies also provide for deductibles, sometimes in the event of theft of up to 25% of the total value of the goods. Of course, a Cargo policy could partially solve the problem, but the general practice shows that normally transport and freight forwarding companies do not have as prerogative the responsibility for insuring the cargoes on first party principle as they are simply not owner of the good.

Check your policies – we can help!

Thus, having above situation, a professional transport and logistics company should make its choice for appropriate provider of insurance solution with broadest possible covers incl. coverage of Willful misconduct (in regards to the critical Art. 29 of CMR) as well as highest possible sums insured depending on the types of cargoes. But not only the wording is critical! The customers must choose out of the several insurance service providers, if possible, a respective so called Assekuradeur like W DROEGE or LUTZ, who are well known for their extensive and profound specialization in Transport & Logistics LoI.

These organisations do not only underwrite the business up to certain limits authorised by risk carriers, they also manage risks and claims to the benefit of the client by involving their loss adjusting partners, lawyer networks and other specialists. A risk carrier is only involved in very high claim and critical cases. They provide trainings and instructions for a better and optimized planning of transport schemes and advise on most critical potential risks.

Be aware and rely on your Transport & Logistics Specialty team!

The tendency of implementing steadily critical regulations is by far not yet over and for this, the industry is rather to be concentrated on actively fitting to new legislation and not passively waiting for insurers to protect them. The transport and logistics companies will further be “squeezed” between new and harder legislation on one side and the creativity of thieves and fraudulent acts within continuous market openness. Together with increased pressure of the ordering parties on our customers this means that we as broker must also act more energetic and steadily improve our offering finding the right insurance and risk solution.

The text is prepared with the special support of former General Manager Otmar Tuma from LUTZ Assekuranz team with excerpts from the Article in „blickpunkt lkw + bus“ Edition 51.

Related Insights

GrECo invests in Corporate Trust to Expand Strategic Risk Management Capabilities

GrECo Group is proud to announce a strategic investment in Corporate Trust, a Munich-based company renowned for its expertise in cybersecurity consulting and classic security business.

Pillar of Our Strategy Is Specialisation – Interview With Georg Winter

Georg Winter offers some insights into his vision for GrECo. Interview was originally published in Lockton Global Partners Magazine.

‘Our only focus is on our client’s and people’s needs’

Ante Banovac shares his thoughts about future risks facing the insurance industry and the state of the insurance market in Serbia, Slovenia and Croatia

Hristo Charkov

General Manager

GrECo Bulgaria

T +359 888 810 100