An effective risk management process is a basic requirement for tackling transformation risks. In most cases, the risk analysis that goes with identifying risks focuses on actual risks. Abstract risks, which are currently hard to assess and thus difficult to evaluate, yet which in essence derive from systemic change or resultant strategic decisions, are often overlooked. However, to master the ever-increasing speed of change we are challenged to adjust the pace with which we tackle the associated risks. Agile risk management plays a decisive role in this process.

My first article of the current HORIZON series introduced our 4 Risk Changers model and put the spotlight on the multiple challenges faced by companies. In the light of ongoing and rapid change, these challenges are to date omnipresent.

Based on our vast experience and extensive expertise in corporate risks, I consider these complex changes as systemic risks. I have categorised them as ecological, geopolitical, technological, and social transformation risks.

Unlike the tangible assets in former years, it is now the intangible assets which increasingly influence the transformation of companies’ risk environment. The major challenges for a forward-looking risk management are posed less by the concrete individual risks at an operating level but more by the abstract systemic risks which are caused by global events and external developments.

Central to my view are the effects of this systemic change on the risk situation of companies. Also, I differentiate between primary and secondary transformation risks.

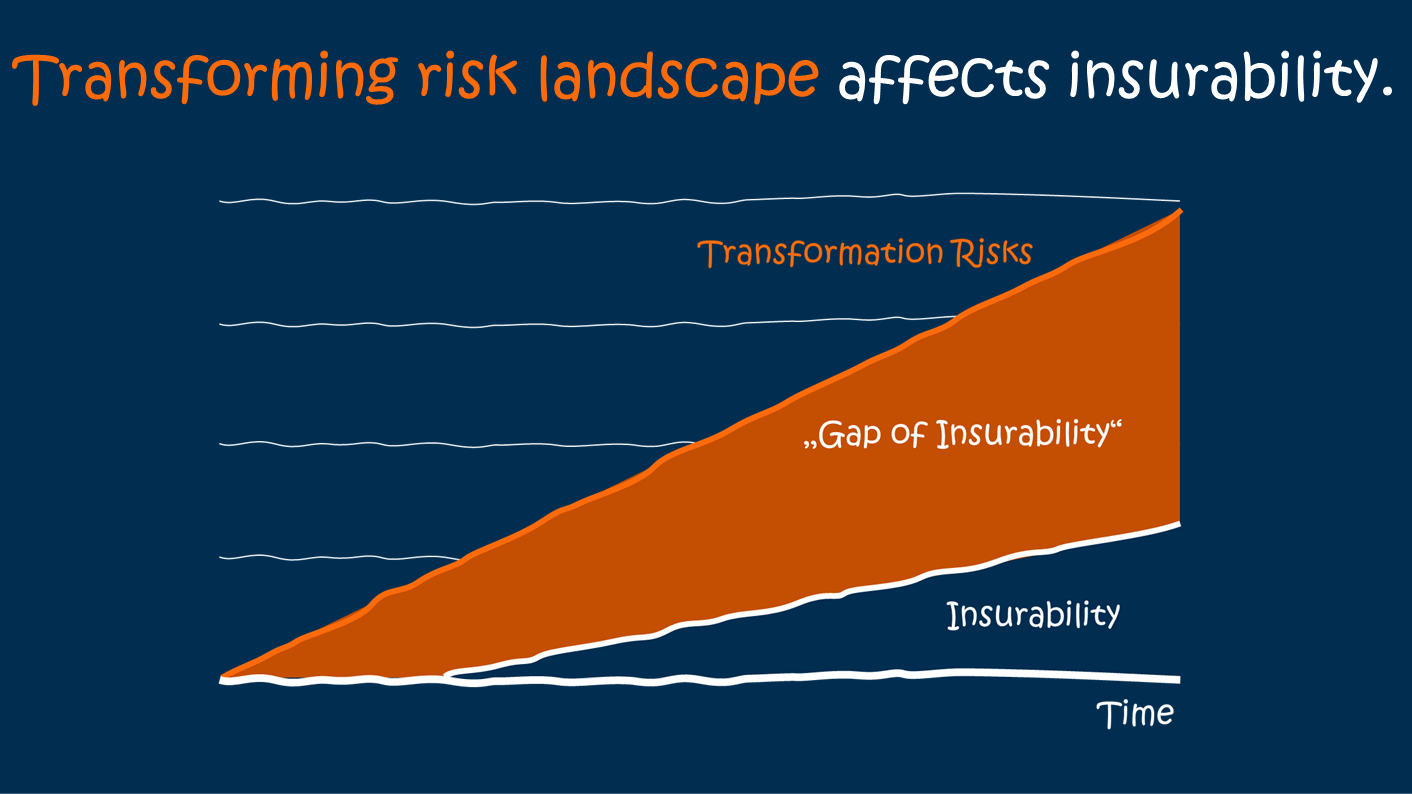

How systemic change affects insurance

Primary and secondary risks tend to increase during a transformation process. They evolve over time. At the beginning, these transformation risks can only be identified with great difficulty. Most of the time we tend to pay less attention to them. Only when they reach a specific threshold, when we become aware of “soft signals”, can they be identified as such and dealt with by risk management.

As is the case with conventional “emerging risks”, the required risk assessment, however, lacks experience, i.e. it lacks historical data and information, presenting an obstacle for analysing transformation risks.

When developing suitable risk management strategies, the attempt to transfer these risks to the insurance market as part of the development of suitable risk management strategies is bound to fail in most cases. The principle of insurability applies. This means, a risk must be measurable for the insurance market to secure adequate capacities. If there is no measurability – as opposed to the maximum loss calculation in the case of fire risks, where the possible maximum loss (PML) represents the maximum expected damage caused – it will be determined based on data modelling of historical risk and claims as well as on actuarial assumptions.

Since new risks and transformation risks lack the required historical data, there is usually also a lack of availability of insurance capacities, especially in their uncertain early stages of development. Adequate insurance solutions (can) only come into being over time.

The current systemic transformation leads to numerous new and changing risks which cause companies’ risk landscapes to change permanently and at an increasingly rapid pace. These dynamics now result in less and less insurance for operational risks, which in the past were adequately and successfully insured.

Thus, as the gap between the lack of insurability and company risks continues to widen, there is an urgent need for the implementation of new methods in risk management.

A transforming risk landscape is often ignored

In practice, many risk management systems that have been implemented only manage concrete risks which already exist. Due to a lack of both early-warning mechanisms and the outside perspective on systemic change and its global events, the risk analysis focus is still on the known and assessable risks. The attention is on the actual situation of the risk environment.

Today’s abstract risks, i.e. risks which still evolve as a result of the changing business environment and have therefore not yet occurred or new risks arising from strategic changes in the business model that aim at seizing new opportunities, are often ignored. In practice, the resultant transformation of the risk landscape is hardly ever anticipated. It is only dealt with once risks manifest themselves because that is when they can be identified and assessed accordingly.

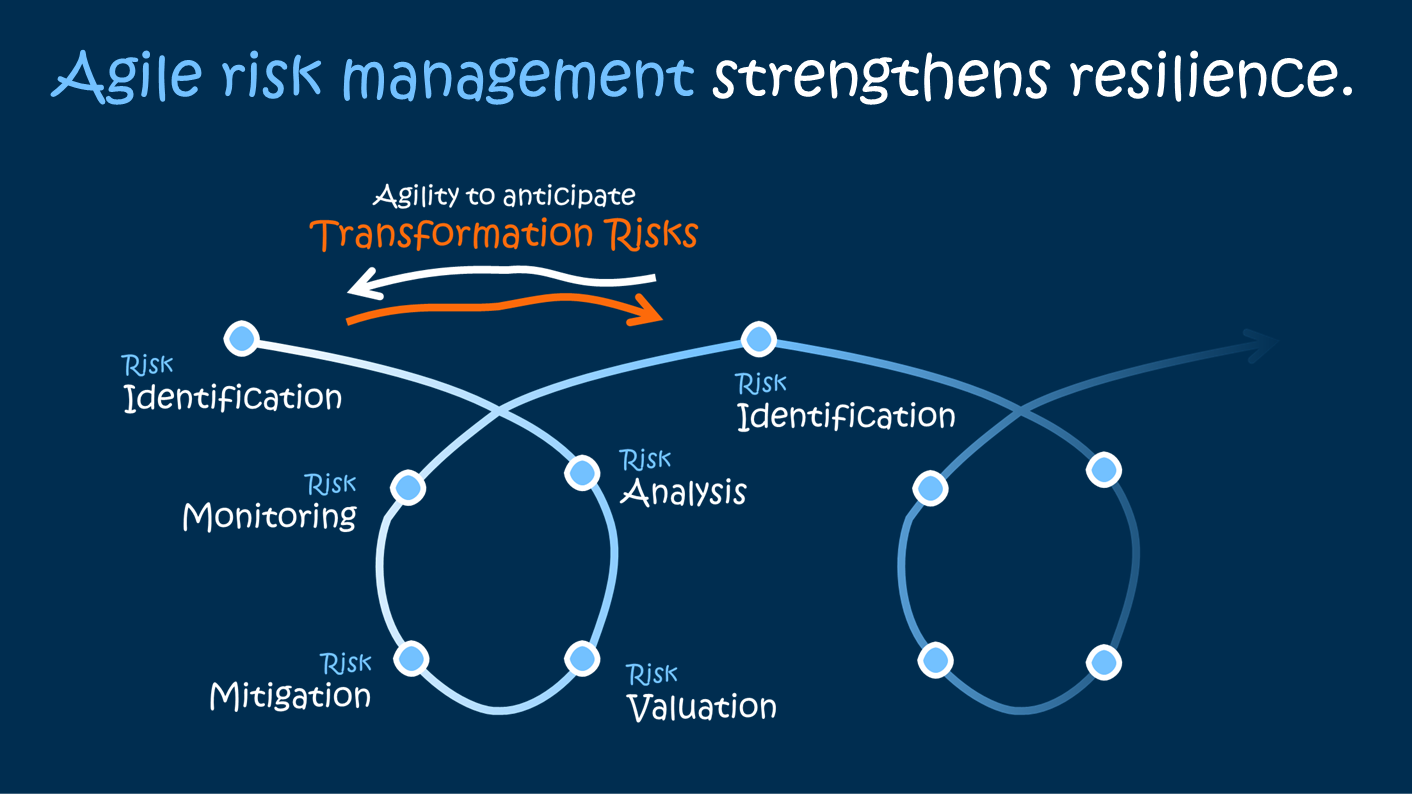

So, how can risk management help to tackle increasing volatility, uncertainty, complexity, and ambiguity and, in turn, boost the resilience of companies? An effective approach that facilitates an agile management of abstract transformation risks needs to be implemented. Existing risk management processes must widen their scope and perspective with some type of risk forecasts, enabling risk managers to anticipate risks at an early stage and allowing them to better prepare themselves.

Agile approach to anticipate transformation

Quite often, we encounter situations where a company’s risk management is organised in closed administrative departments which function like silos that were put in place to comply with legal requirements. Because such risk management deals with risks at an individual level only, its benefit as a company-wide tool to effectively manage risks often fails to achieve its full value.

The agile management of risks and opportunities is based on a corporate culture that is open-minded towards such risks and opportunities and is organised around transparency, dialogue, trust, and constant feedback cycles.

It comprises interdisciplinary teams whose members act with utmost flexibility as and when needed and who are an integral part of strategic and operative decision-making processes.

That way, transformation risks can be anticipated and acted upon at an early stage. This boosts the resilience of companies, enabling them to make the most out of future opportunities.

Anticipating transformation risks at an early stage means viewing the world from a future perspective and interpreting the inherent risk situation in the best possible way. Paying attention to soft signals, like new and shifting trends, as well as an open-minded attitude towards strategic considerations helps the establishment of effective early-warning indicators to manage risks.

Agility drives insurability and strengthens resilience

As a risk specialist, it is our vision to manage the risks of our clients in such way that they can rest assured and focus on their core business.

As a loyal and trustworthy partner, we work for and with our clients in flexible, interdisciplinary teams where we prove our transparent, dialogue-driven culture every day.

We anticipate systemic change and proactively direct our organisation towards the future needs of our clients. Agile risk management plays a key role for us.

In future, our progressive service approach will focus even more strongly on anticipating any change and resultant risks at an early stage.

HORIZON – “Risk Thought » Fast Forward” is our platform for risk-thought leadership. It follows our ambition to anticipate systemic change at an early stage, drive the insurability of a transforming risk landscape and create value through tailored solutions that strengthen our clients’ resilience and protect their future ventures.

GrECo, matter of trust.

Georg Winter

CEO GrECo Group

T +43 664 962 39 06

Related articles

Fringe Benefits Are Reshaping the Employment Offer

Unlike core benefits such as medical care or pensions, fringe benefits are often the most visible to employees.

The Benefit Everyone Wants, But Nobody Structures the Same Way

For employers wanting to ensure their Health & Benefits strategy delivers real value over time, our Study has made it clear that those who focus on an informed approach that combines market understanding, structural comparison and local relevance will succeed.

We Say Yes to Net Zero

GrECo Austria’s Roland Litzinger sat down with the CEO of delfort. Martin Zahlbruckner, to discuss how a global specialty-paper group is driving emissions reductions.