According to the International Monetary Fund food and energy are the main drivers of today’s inflation. That is obvious to each of us as we pay more for both food and energy these days.

This article compares the food price inflation in the countries of Central and Eastern Europe where GrECo Group operates. How did these differences in prices come about and what are the consequences for insurance?

How food price inflation is measured

The United Nations’ Food and Agriculture Organization uses the Food Price Index (FFPI) to track and monitor price changes in international markets for key basic foodstuffs. The reference period from 2014 to 2016 serves as the FFPI base value, this being 100. For example, if in July 2005 the FFPI in Austria was 76.4, this means that the main basket of food products cost 23.6% less in July 2005 than the average basket in 2014-2016yy. If the FFPI, let’s say, in June 2022 was at 121.1, the food inflation was 21.1% compared to 2014-2016yy.

Different rates of food price inflation in Europe

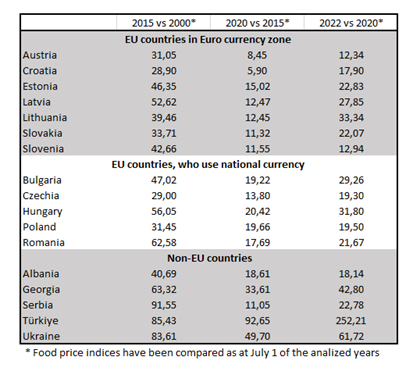

We analysed the food price indices in CEE/SEE countries, which are split into 3 groups:

The analysis shows that the increase in food prices in EU countries follows the same course, i.e. the dynamics from 2020 are very high compared to the previous 20 years (2000-2019yy). This proves that the economies of EU countries are interconnected.

Looking at countries outside the EU, we see that prices have risen in different ways at different times. For example, an interesting fact about Ukraine is the sharp increase in prices in 2013-2014, which can be attributed to the destabilisation of the economic situation during the Maidan Revolution, followed by the first Russian occupation and the subsequent large devaluation of the local currency.

A more interesting trend can be seen if we take a closer look at the period 2020-2022, primarily related to COVID and Russia’s invasion of Ukraine.

A look at increasing food prices during 2020-2022

The table below clearly illustrates the differences between countries. It allows for a better comparison of FFPI values at different points in time during recent periods. For example, the column 2022vs2020 shows the percentage increase in food prices on July 1, 2022 as compared to July 1, 2020.

The table also shows that inflation in the period 2022-2022yy was twice as high as in the period 2020-2015yy in almost every country. Prices started to increase drastically as from the third and fourth quarter of 2021. We therefore believe that the root cause was the post-COVID food and energy supply chain crisis.

Why is food price inflation so high in 2020-2022?

One of the root causes of any inflation is the scarcity of goods, eithertheir total lack or their availability in only insufficient quantities. This happened in the post-COVID recovery phase, when deferred demand for energy resources collided with supply chain constraints. At the same time, in 2021, we witnessed a sharp increase in the prices of cereal and oilseed raw materials. We also saw the first forecasts of increasing food prices. Soon thereafter, Russia’s invasion of Ukraine led to a new problem in the food supply chain, a problem that continues to this day.

Another cause of inflation is excess demand, be it due to the government printing extra money, the acceleration of the money multiplier, new demand created by GDP growth or due to the inflow of new foreign capital. For example, according to Forbes the consistent monetary stimulus on a massive scale, unprecedented since World War II, turned the flywheel even further in 2020-2022.

On top of that, the negative expectations of enterprises and consumers add even more fuel to the fire. Today, nobody is willing to take a risk by selling goods without hedging against the risk of higher production costs in the future. Already, manufacturers are increasing their prices in order to transfer the risk to their consumers. There is also the theory, that big corporations and monopolists (e.g. in the energy segment or food retail) merely squeeze out more profit by driving prices up. Therefore, it will be interesting to see what the final 2022 balance sheets and ESG reports will look like in 2023.

Impact of the inflation on the insurance markets

In our opinion, inflation impacts negatively on insurance consumption and insurance premiums. On the positive side, greater financial uncertainty and changes in the spending behaviour (increased share of spending on inflexible goods and utilities) make households and enterprises rethink their insurance spending.

To further curb price increases, central banks significantly raised base rates. Together with inflation expectations and the calculation of an additional risk premium for uncertainty, such actions lead to a significant increase in the cost of capital. This means that investors in the insurance industry are increasingly making outrageous demands.

Thus, we have already witnessed a lack of capacity following the first wave of investor capital outflow from international insurance markets. As a result, insurers are not only starting to optimise their portfolios, they are also becoming increasingly risk averse. Some of the conventional property risks are very difficult to renew and additional limits in e.g. the meat industry, in agricultural insurance, and in other sectors can hardly be obtained. Markets are thus hardening again.

What can we expect in the near future and what will save us from the abyss?

Food and energy supply chain constraints pushed up prices post-COVID. Aggressive government monetary policies, negative expectations and further supply chain disruptions caused by Russia’s invasion of Ukraine exacerbated the situation. This has affected the countries of the CEE/SEE region in different ways, yet what they have in common is that prices in 2021-2022 have soared at an unprecedented rate. The insurance market, in turn, is entering a phase of portfolio optimisation due to the growing lack of investor capital.

So, what does the future have in store for us?

A similar scale of inflation (as shown in the graph below) took place in the 1970s when price increases were associated with oil shocks in 1973 and in 1979-80. That said, prior to these shocks, monetary policy was focused on keeping interest rates low to maintain employment levels and pour more money into an economy that resembles ours today. Further policy tightening resulted in a deep economic crisis in the early 1980s.

However, there are two important differences between the current situation and the 1970s:

According to The Centre for Economic Policy Research (CEPR) “beyond the near term, inflation is expected to decline, but the experience of the 1970s suggests some material risks to this inflation outlook”. CEPR considers risks to be material if the following events do not occur: ”1. global production lines and logistics adjust, 2. inflation expectations are likely to remain well anchored over the medium term, 3. the structural forces that depressed inflation before the pandemic persist”.

In addition, we believe that increasing economic activity towards the reconstruction of Ukraine and new investments in technologies leading to the decarbonisation of economies will additionally inject economic growth, which will in turn, result in a stabilisation of prices.

Sources consulted:

https://www.fao.org/datalab/website/web/food-prices

https://www.forbes.com/sites/georgecalhoun/2022/09/30/what-is-really-driving-inflation-today/

https://www.fao.org/faostat/en/#data/CP

https://www.imf.org/en/Blogs/Articles/2022/09/09/cotw-how-food-and-energy-are-driving-the-global-inflation-surge )

https://cepr.org/voxeu/columns/todays-inflation-and-great-inflation-1970s-similarities-and-differences

Related Insights

GrECo invests in Corporate Trust to Expand Strategic Risk Management Capabilities

GrECo Group is proud to announce a strategic investment in Corporate Trust, a Munich-based company renowned for its expertise in cybersecurity consulting and classic security business.

Pillar of Our Strategy Is Specialisation – Interview With Georg Winter

Georg Winter offers some insights into his vision for GrECo. Interview was originally published in Lockton Global Partners Magazine.

‘Our only focus is on our client’s and people’s needs’

Ante Banovac shares his thoughts about future risks facing the insurance industry and the state of the insurance market in Serbia, Slovenia and Croatia