Since the 1990s, countries of Central-, Eastern-, and Southeastern-Europe have largely been transitioning to market economies with democratic forms of government and now participate in global markets for goods and services.

Starting of the Transition

The general transition also concerned the insurance market. Drastic changes had to be made to break insurance monopolies which were in place during the communist era as part of fiscal authorities. Existing insurers were first converted into state-owned companies and then privatized. While this transition was taking place, also new, privately-owned insurers appeared on the markets in all parts of Central and Eastern Europe. However, the former monopolists held on their dominant market share for several years and in some markets are still the major players. This transition was characterized by the high pace of foreign direct investments, also into the insurance market. The number of insurers controlled abroad remains high, even today.

Joining the European Union

One additional major factor in the development of the insurance markets is also the accession to the European Union. By today, most of the countries in CESEE have joined, or are in discussion to join, the EU. Accession compelled the adoption of European Union standards including the ban on state monopoly, liberalization of market access, abolition of price and product controls, as well as finance-related issues such as adoption of EU solvency regulations, tightening of capital adequacy requirements and strengthening insurance market supervision. This included full market access for companies from other EU members which translates to regular use of Freedom of Service coverages in those countries.

Despite the rapid transition towards a free and fully EU-compliant insurance market, the insurance density and insurance penetration are significantly below Western European standards. For example, annual insurance premium per capita is above 2.000 EUR in Austria and in Eastern Europe only between 50 in Albania and 1.000 in Slovenia with an average of 450 EUR.

Main players and impact of foreign insurance groups

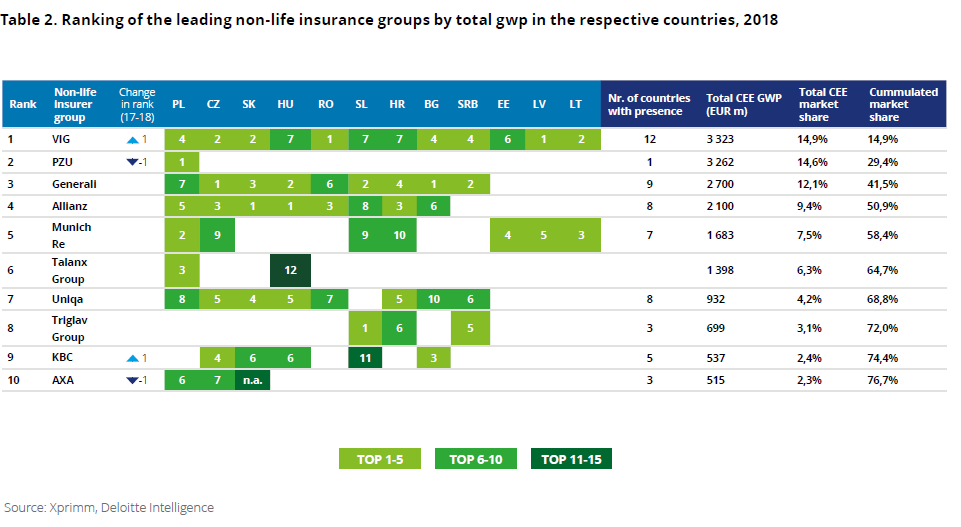

During and prior to accession the impact of foreign insurers was significant, as most insurance market leaders in the countries joining the EU in 2004 were owned by foreign companies with Allianz as leading foreign insurance group being the prime example. As of 2018, the major insurance group in CEE is Vienna Insurance Group (VIG) with a presence in 21 countries and a GWP of more than 5 billion EUR in those countries. Of the Top 10 non-life insurance groups operating in Eastern Europe eight are foreign owned. The same goes for the life insurance sector.

The major local players are PZU in Poland and Triglav in Slovenia which both have their roots in state owned monopolies from the communist area. The main foreign investments in the Eastern European insurance markets stem from Europe, namely Austria, Germany, Italy, France and Benelux. Other, less prominent players are groups from the US, Canada and the UK.

Consolidation of the insurance market

In recent years, a trend towards consolidation can be observed. This is due to the very granular structure of the market with multiple rather small countries and unfulfilled growth expectations.

One recent example is Uniqa’s acquisition of the AXA subsidiaries in Poland, the Czech Republic, and the Slovak Republic. This 1 billion EUR merger further strengthens Uniqa’s footprint in Central Eastern Europe while concluding AXA’s withdrawal from the region. “For us, the growth markets in Central and Eastern Europe are our second home market. With the purchase of the AXA companies, the profitable retail business and balanced product mix perfectly match our long-term growth strategy, we are now one of the leading insurance groups in the CEE region,” comments Andreas Brandstetter, CEO of UNIQA Group.

On November 29th 2020, Vienna Insurance Group signed a share purchase agreement to acquire the entities of the Dutch insurer AEGON in Hungary, Poland, Romania and Turkey.

“The acquisition of the Central and Eastern European business of Aegon is an important step for our Group to sustainably strengthen our leading position in CEE and to take advantage of new opportunities. In Hungary, we are making the leap to the top. In Turkey, we succeed in entering the life insurance market and in Poland, Romania and Hungary we can significantly expand our potential in the pension fund business,” says CEO Elisabeth Stadler about the successful deal with Aegon.

Smaller mergers and acquisitions in 2020 happened in various other countries, such as Romania, where Allianz acquired Gothaer Romania.

Increasing Interest for Corporate Insurance

The insurer landscape and insurers’ risk appetite is undergoing dynamic developments in the CEE region. While the main focus for insurers remains on profitable private lines and standard product offerings for small businesses, an increasing interest for corporate risks can be observed also among pure local insurers.

Due to relatively moderate local capacities and consequently relatively low retentions, usually ranging between 20 and max. 50 million EUR depending on the risk, structured reinsurance is regularly needed when incorporating covers. This trend is expected to continue as corporate clients’ risk awareness increases. Sometimes it reaches Western European standards already today. This will most likely pave the way for specialty risk advisory to become more sought after in the years to come.

30 years of experience in CEE

GrECo has been operating successfully in CEE for over 30 years and today is the leading corporate risk advisor and insurance broker in the region. Over the decades close ties to group management of all insurance companies in the region have been established and are being constantly nurtured. This is the basis for swift and competitive implementation of sophisticated tailored covers for our clients.

With our strong presence in 16 countries via owned offices, excellent insurer relations and profound operational expertise GrECo is in a prime position to deliver first class specialty placements. Our international expertise also allows us to implement fronting solutions for multinational clients efficiently. This is making us the first choice for independent international partners around the world.

We have experienced the transitions of the insurance markets first hand. Having been in the region for over 30 years we have gained insights we are happy to share with our partners.

Related Insights

GrECo invests in Corporate Trust to Expand Strategic Risk Management Capabilities

GrECo Group is proud to announce a strategic investment in Corporate Trust, a Munich-based company renowned for its expertise in cybersecurity consulting and classic security business.

Pillar of Our Strategy Is Specialisation – Interview With Georg Winter

Georg Winter offers some insights into his vision for GrECo. Interview was originally published in Lockton Global Partners Magazine.

‘Our only focus is on our client’s and people’s needs’

Ante Banovac shares his thoughts about future risks facing the insurance industry and the state of the insurance market in Serbia, Slovenia and Croatia