Interesting facts about forests, the risks associated with them, and a little about how to insure them

Forestry insurance is still undervalued but can be a really good tool to reduce losses in the wood-processing supply chain. This year, it has become relevant especially for tourism in some countries where wildfires have created activity restrictions in specific areas.

Forest world

It is estimated that nearly 1/3 of the global population depends on forest goods and services for livelihoods, food security and nutrition. Tree stands outside forests contribute to the four dimensions of food security (i.e. availability, access, utilization and stability) by providing income, employment, energy, ecosystem services and nutritious foods.

Globally, about 1.15 billion ha of forest are managed primarily to produce wood and non-wood forest products. In addition, 749 million ha are designated for multiple use, which often include the production. Forestry is an integral part of the wood-processing industry. There is less and less natural forest on earth. On the other hand, the growing new plantations are developing very well. Many big wood-processing companies started doing vertical integration of their traditional facilities with forestry in order not to be fully dependent on external suppliers.

Source: Global Forest Resources Assessment 2020 – Key findings. Rome: FAO. 2020.

The area of naturally regenerating forests has decreased since 1990 (at a declining rate of loss), but the area of planted forests has increased by 123 million ha.

Forests cover nearly 1/3 of land globally. That is 4.06 billion hectares. In other words, there is around 0.52 ha forest for every person on the planet. More than half (54%) of the world’s forests are in just five countries: the Russian Federation, Brazil, Canada, the United States of America and China. 93% of the world’s forest area consists of naturally regenerating forests and 7% is planted.

Source: Global Forest Resources Assessment 2020 – Key findings. Rome: FAO. 2020.

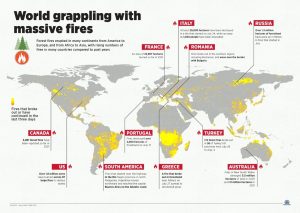

More and more damage to forests

Forests face many disturbances that can adversely affect their health and vitality and reduce their ability to provide a full range of goods and ecosystem services. For example, about 98 million ha of forest were affected by fires in 2015. Insects, diseases and severe weather events damaged about 40 million ha of forests in 2015, mainly in the temperate and boreal domains.

The world’s climate is changing. Increased temperatures and levels of atmospheric carbon dioxide as well as changes in precipitation and in the frequency and severity of extreme climatic events are just some of the consequences. These changes are having a remarkable impact on the world’s forests and the forestry sector, e.g. through longer growing seasons, shifting ranges of insect pests and an increase of forest fires.

For example, in 2019 in Europe and MENA regions fires of greater than 30ha were observed in 40 countries and a total burnt area of 789 730 ha was mapped, which is nearly four times more than in 2018.

More and more damage to forests

Source: Wildfires ravaging forestlands in many parts of globe

Stormy seasons

Climate change is not only associated with dry days and high temperatures, but also with more catastrophic wind speeds. The main losses are therefore damage to timber, pulp and logging, restoration costs and the loss of production capacity on forest land.

Source: Biggest windthrow volumes

There are various scenarios of damage after the storm:

Secondary losses resulted by storms:

Forestry insurance

As for insurance, 2/3 of forests are insured under property policies, 1/3 of forests are insured under forest policies. The premium volume is estimated at around USD 150 million. The insurance cover is about 10% of all plantings

Source: SwissRe forestry presentation (agriinsurance conference in Istambul 2018)

The main risks that are covered by standard forestry “damage-base” insurance is fire, lightening and windstorm. Additionally, hail, ice, snow, flood and earthquake can be insured. Pests & diseases are main exceptions from the coverage but can be additionally indirectly insured via parametric insurance if there is strong correlation between the weather factor and the occurrence of higher pest populations and the spread of diseases.

There are several approaches to assessing the sum insured:

Parametric forest insurance

Hurricane and forest fire risks can also be insured with parametric policies. Storm data are usually provided in the form of wind speed maps by independent private data providers. Based on this, the insured area will be divided into different speed zones. For each speed zone, a certain fixed indemnity is determined according to the insurance contract.

Regarding parametric fire insurance, data on burned-out areas can be provided from satellites (MODIS, Sentinel, etc.), based on the actual value of the insurance index is determined. The trigger for this policy is the minimum burn-out area.

Related Insights

GrECo invests in Corporate Trust to Expand Strategic Risk Management Capabilities

GrECo Group is proud to announce a strategic investment in Corporate Trust, a Munich-based company renowned for its expertise in cybersecurity consulting and classic security business.

Pillar of Our Strategy Is Specialisation – Interview With Georg Winter

Georg Winter offers some insights into his vision for GrECo. Interview was originally published in Lockton Global Partners Magazine.

‘Our only focus is on our client’s and people’s needs’

Ante Banovac shares his thoughts about future risks facing the insurance industry and the state of the insurance market in Serbia, Slovenia and Croatia