One thing is clear – Europe needs to cover gas demand with alternative sources. The EU energy security is compromised if there is no diversification to cover Russian gas imports. EU gas imports account for over 1,500 TWh and need to be switched into an alternative source.

Energy security concerns are sparking lively debates not only in the politicians’ offices, boardrooms, and conferences. This topic has made its way to family dinner tables, parties, and pubs. There are wild stories to be heard with opinions being polarised and swaying in both directions. Although it may seem that we are facing the impossible task of shifting from fossil fuels to renewable energy sources, public polls actually show a high degree of consent (9 out of 10 Europeans agree) regarding the EU’s energy policy priorities to ensure secure, clean, and affordable energy for all Europeans, according to a new Eurobarometer survey published by the European Commission.

The main questions are evolving around the feasibility of energy transition and the corresponding timeline. It is not a matter of if, but how and when. Our Energy, Power & Mining team looked closer into this issue.

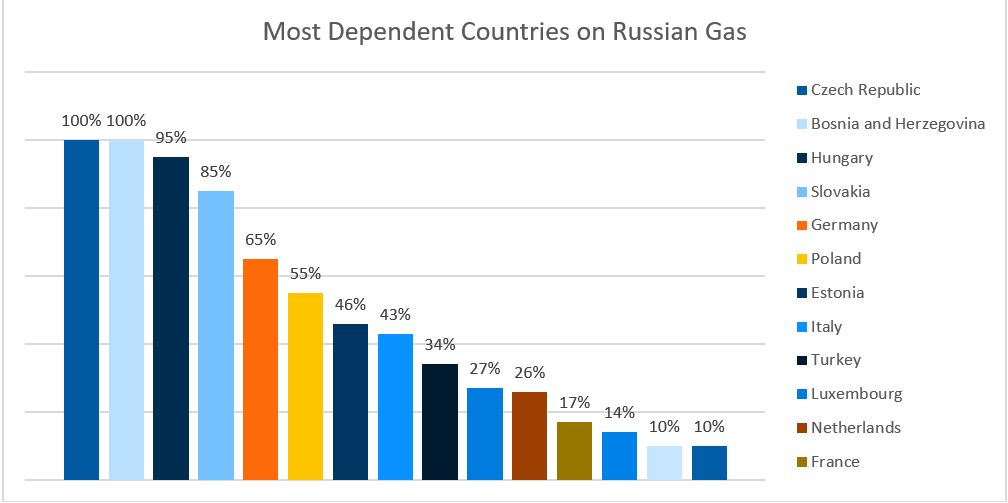

As of March 2022, 85% of the EU gas demand was imported. Thereof 34% came from Russia and only 17% from Norway. The dependency on Russian gas has grown significantly within the EU, some countries being fully dependent on the single source, as the diagram below indicates.

Source: GlobalData, Eurostat

Over 30% of the imported Russian gas is being used for power and heat generation, and an additional 25% is used by the residential sector followed by industrial production with 21%. It is hardly a surprise that Russia’s ability to weaponise energy only accelerated pressure on consumer prices, global supply chains and the labour market.

The road towards alternative energy sources

One thing is clear – Europe needs to cover gas demand with alternative sources. The EU energy security is compromised if there is no diversification to cover Russian gas imports. EU gas imports account for over 1,500 TWh and need to be switched into an alternative source.

The International Energy Agency (IEA) has elaborated a 10-point plan for Europe. The plan is divided into 4 major action fields as follows:

Gas oriented actions

Energy efficiency oriented actions

Renewables oriented actions

Market oriented actions

Research shows that the successful implementation of the plan can eliminate the demand for Russian gas by 2030. The renewable share of Energy has been growing steadily since 2004 currently reaching 23%. Hydrogen is perceived as a support to the gas sector. Renewable Energy Directives (RED) are assessing the possibility of installing blending obligations for increasing the sustainability of the European gas system from currently 1% to 20%, but not without major grid and infrastructure adjustments.

Apart from reducing the dependency on Russian gas, which now seems possible, there are various other aspects of the energy transition to consider as well. But for the moment, keep calm and follow the plan. So far so good.

What about the risks?

We read and hear surprisingly little about the uncertainties, unknowns, and associated project risks of such undertaking. Known unknowns are what drive many scientific experiments, business intelligence and data analytics and refer to information whose existence is someone aware of but does not possess. They can also represent potential risks. They can also represent potential risks. Far worse are the unknown unknowns, pieces of unidentified information, or “things we do not know that we don’t know”.

The plan addresses several items, which carry inherent limitations in their nature and can, therefore, be considered severe project risks. For example, selling and installing 30 million heat pumps in the shortest term possible is a challenge even without limited manufacturing capacity globally, supply chain pressure and logistical difficulties.

Accelerating renewable energy generation capacity (EU requires over 900 TWh additional capacity by 2030) seems extremely unlikely for the reasons mentioned above and impossible without the addition of new manufacturing facilities, ideally closer to home, and not overseas. This means that technical and technological sacrifices will need to be made to accomplish the colossal task in a very short period. Furthermore, new personnel must be hired and trained to a very high standard demanded by the ever-increasing complexity of the renewable generation machinery (especially wind turbines). The recent crises caused by post-COVID shortages of staff in European road transport and air travel industries demonstrate just how difficult is to mobilise and ensure the supply of qualified labour to meet the demands of the green energy business.

Also, the grid, gas transport and storage infrastructure will require more than a major overhaul to adopt hydrogen blending due to the physical and chemical properties of hydrogen (highly corrosive, existing networks were not built with that in mind).

Lastly, it would be interesting to read the estimates of the capital expenditure required to upgrade the entire EU’s transmission and distribution grid systems to accommodate the change of topology coming from the replacement of a small number of centrally dispatched generation assets (located near the largest industrial electricity users) by a large number of distributed renewable sources located across the entire continent and in the neighbouring seas.

Until then, Europe will have to keep its coal-fired plants going (for example, Germany has already initiated a legal proceeding to abolish the prohibition of operating thermal coal plants beyond 2022-23).

Besides, 2030 is still 7.5 years away, yet the winter will be upon us in just a few months.

Related Insights

GrECo invests in Corporate Trust to Expand Strategic Risk Management Capabilities

GrECo Group is proud to announce a strategic investment in Corporate Trust, a Munich-based company renowned for its expertise in cybersecurity consulting and classic security business.

Pillar of Our Strategy Is Specialisation – Interview With Georg Winter

Georg Winter offers some insights into his vision for GrECo. Interview was originally published in Lockton Global Partners Magazine.

‘Our only focus is on our client’s and people’s needs’

Ante Banovac shares his thoughts about future risks facing the insurance industry and the state of the insurance market in Serbia, Slovenia and Croatia